That First Salary Moment Nobody Talks About Honestly

You remember your first salary, right? That moment when the amount hit your account, and you sat there thinking, okay, now what? Most people, if we’re being real about it, spend it. Maybe a little goes to family, a little to rent, a little to that long-pending phone upgrade. And somewhere in the shuffle, “investing” becomes this vague promise you make to your future self. Next month, you say. I’ll start next month.

Now here’s the thing. That next month eventually becomes a decade. And suddenly you’re thirty-something, maybe forty, still telling yourself you’ll figure it out later. The problem isn’t willpower. It really isn’t. The problem is that nobody showed you a simple picture of what starting small and growing steadily actually looks like over time. That’s where a Step-Up SIP Calculator quietly walks in and changes everything.

What Even Is a SIP, and Why Should You Care

Let’s not assume everyone’s on the same page. A Systematic Investment Plan, or SIP as most people call it, is basically a commitment you make to invest a fixed amount every month into a mutual fund. Think of it like an EMI, except instead of paying off debt, you’re building wealth. You pick an amount, you pick a fund, and every month, that money moves automatically. You don’t have to think about it. You don’t have to time the market. You just stay consistent.

Read More : How Digital Gold Loan Applications Cut Branch Processing Time

Simple enough. But here’s where most people stop. They set up a SIP for, say, two thousand rupees a month, feel great about it, and forget to revisit it. Years pass. Their salary doubles, maybe triples. But the SIP? Still chugging along at two thousand. Hasn’t moved. And now that two thousand, which once felt like a decent contribution, is barely a rounding error in their monthly income. See the problem?

The Step-Up Idea, Which Is Honestly Just Common Sense

A step-up SIP, sometimes called an escalating SIP, is exactly what it sounds like. You don’t invest a flat amount every year. Instead, you increase it by a certain percentage, usually somewhere between five and twenty percent, every year. So, if you start at two thousand this year, you move to maybe twenty-two hundred or twenty-four hundred next year, and so on. Gradual. Not painful. Completely in sync with how salaries actually work in the real world.

Think about it. Every April, most salaried folks get an increment. Maybe it’s ten percent, maybe it’s fifteen. That increment lands in the account and, well, lifestyle inflation being the sneaky thing it is, it gets absorbed pretty quickly. A slightly nicer dinner out. An upgrade in grocery choices. A streaming subscription or two.But compound that spending over ten years, and you’ve essentially let a significant chunk of your income evaporate into thin air.

What if, instead, even half of that annual raise went into your investment? That’s the core idea behind step-up investing, and it’s not some radical financial philosophy. It’s just sensible. Incrementally grow your savings in proportion to your income. Match your financial ambition to your actual earnings trajectory.

Hold On, Let Me Think About That Calculation for a Second

Because the moment anyone starts talking about compound interest and annual increments and fund returns, the brain starts doing that thing where it pretends to listen but actually isn’t. The numbers feel abstract. Distant. Not real.

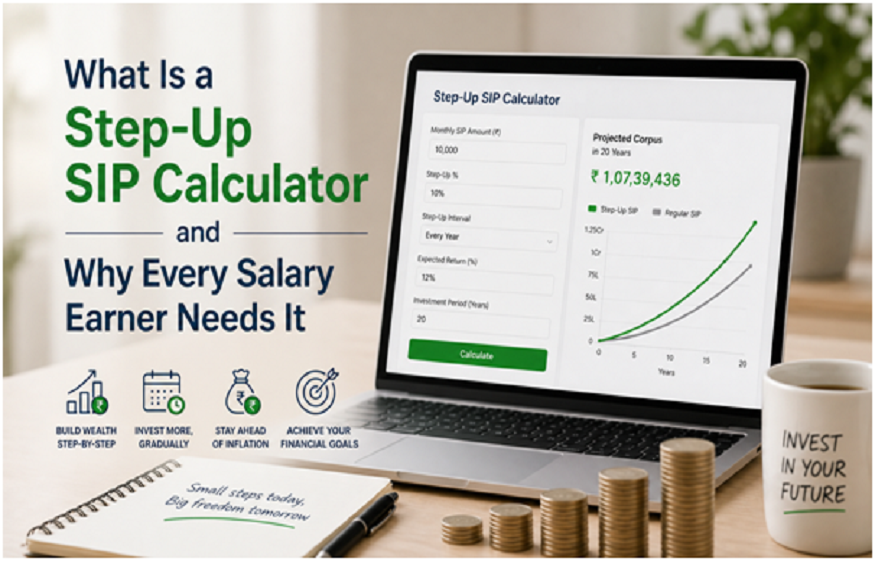

This is precisely why the Step-Up SIP Calculator exists. It’s a tool, usually found on financial portals and fund-related websites, that lets you plug in a few numbers and instantly see what your money could look like after ten, fifteen, or twenty years. You enter your starting monthly investment, your expected annual increase percentage, the anticipated rate of return, and the time horizon. Hit calculate. And out pops a number that, honestly, tends to make people sit up a little straighter.

Let’s walk through a rough example, without getting too textbook-y about it. Say someone starts a monthly SIP of three thousand rupees at age twenty-five. Standard SIP, no step-ups. Assuming a twelve percent annual return over twenty-five years, they’d accumulate somewhere in the range of one and a half crore rupees. Not bad at all.

Now apply a ten percent annual step-up to that same SIP. Same starting amount. Same return assumption. Same timeframe. The final corpus jumps to somewhere around four to five crores. That’s not a small difference. That’s nearly three times the wealth from a tweak that, in the early years, meant increasing your monthly investment by maybe three hundred rupees.

Why Salary Earners Specifically Miss This Trick

Salaried professionals are, statistically, the most disciplined investors. They have a predictable income. They’re more likely to set up auto-debits. They actually show up for the long game. And yet, ironically, they’re also the group most likely to set a SIP and forget it for the next fifteen years without ever scaling it up.

Why? Partly inertia. Partly because nobody reminds them. Partly because the paperwork of modifying a SIP feels oddly daunting, even though it takes about four clicks on a phone. But mostly, I’d say from experience of talking to people about this, it’s because they don’t see the difference it makes. What’s the point of increasing by five hundred rupees? It feels trivial.

A good annual increment calculator shows you exactly what point. And once you see those numbers laid out, the five hundred rupees stops feeling trivial. It starts looking like a down payment on a different retirement.

How the Calculator Actually Helps You Plan Better

Here’s what most people do wrong when they think about long-term money goals. They pick a big, round target and work backwards with a flat monthly investment. Want one crore in fifteen years? Okay, put in X amount per month. Fine. That works, technically. But it assumes your financial situation never evolves, which is… not how life goes.

The beauty of using a step-up calculator is that it lets you plan dynamically. You can model different scenarios. What if I start small now but increase aggressively every year? What if my increments slow down at some point? What’s my corpus if I invest for twenty years versus twenty-five? These aren’t hypothetical exercises. They’re genuinely useful for setting a goal, picking the right starting amount, and deciding how much to increase annually.

It also, and this part matters, removes the guilt from starting small. One of the biggest reasons people delay investing is that they feel like they don’t have “enough” to make it worthwhile. A few thousand a month seems laughable against a goal of a crore or more. But when you see how a modest start combined with annual step-ups compounds into something genuinely significant, it reframes the whole conversation. Start now. Increase every year. Trust the math.

The Emotional Side of Watching Your Money Grow

Now, I don’t want to sound like a financial brochure here, so let me be honest. There’s something genuinely motivating about seeing projections. Not because the numbers are guaranteed, they aren’t, markets do what markets do, and no calculator can predict the future with precision. But seeing a plausible, reasoned estimate of what disciplined investing looks like over twenty years does something to your relationship with money.

It makes it feel worth it. It turns the abstract into the concrete. And honestly, for most people who grew up watching their parents worry about money rather than grow it, that shift in perspective is no small thing. It’s almost psychological. You stop treating investing as a sacrifice and start treating it as a choice you’re making for your own future self.

A Few Practical Thoughts Before You Jump In

You don’t need a financial advisor to start using one of these tools. Most investment platforms have a version of it built in. It’s free. It takes maybe five minutes to play around with. Put in your current SIP amount, or the amount you’re thinking of starting with. Assume a ten to twelve percent annual return, which is a reasonable long-term expectation for equity mutual funds historically, though again, no guarantees. Set your annual step-up at ten percent, roughly aligned with typical salary hikes. Choose your investment horizon.

Then look at the number. Really look at it. And then look at what happens if you delay starting by just three years. That gap tends to be sobering.

One thing worth mentioning: don’t get obsessed with squeezing the highest possible return assumption into the calculator. It’s tempting to punch in fifteen or eighteen percent and watch the final corpus balloon into something magnificent. But that’s not planning, that’s fantasy. Be conservative. Be realistic. A Step-Up SIP Calculator is only as useful as the assumptions you feed it.

The Quiet Power of Starting Before You’re Ready

Here’s the uncomfortable truth. Most people never feel fully ready to invest. There’s always a reason to wait. The loan isn’t paid off yet. There’s a vacation coming up. The market seems uncertain. The timing feels off. Life, with all its lovely unpredictability, is remarkably good at providing excuses.

Read More : Fixed Deposit vs Savings Account: What Should You Pick for Short-Term Goals?

But wealth is built by the people who started before they felt ready. Who began with amounts that felt embarrassingly small. Who increased steadily, year after year, not because they were disciplined saints but because they set up a system and let the system do its thing. The SIP investment calculator doesn’t just show you numbers. It shows you a version of your financial life where the decisions you make today compound, literally and figuratively, into something worth having.

Every salary earner deserves to see that picture. Not because it’s guaranteed, but because it’s possible. And that possibility, grounded in a bit of math and a lot of consistency, is worth every minute you’d spend with a calculator figuring it out.